Lunatics!

Lessons from the Terra journey to the moon and back.

Hi! It’s George from Investorama. Welcome to the new joiners.

I wrote about Stablecoins earlier, and it deserves to be revisited following the demise of UST (Terra USD), the algorithmic stable coin from the Terra protocol.

It’s a rare opportunity for investors (across traditional and crypto markets) to witness the meteoric rise and fall of a project whose design was unsustainable. And there’s a lot for founders and marketers too.

Given what we know now, the main question about Terra is not what went wrong but what drove it to the moon.

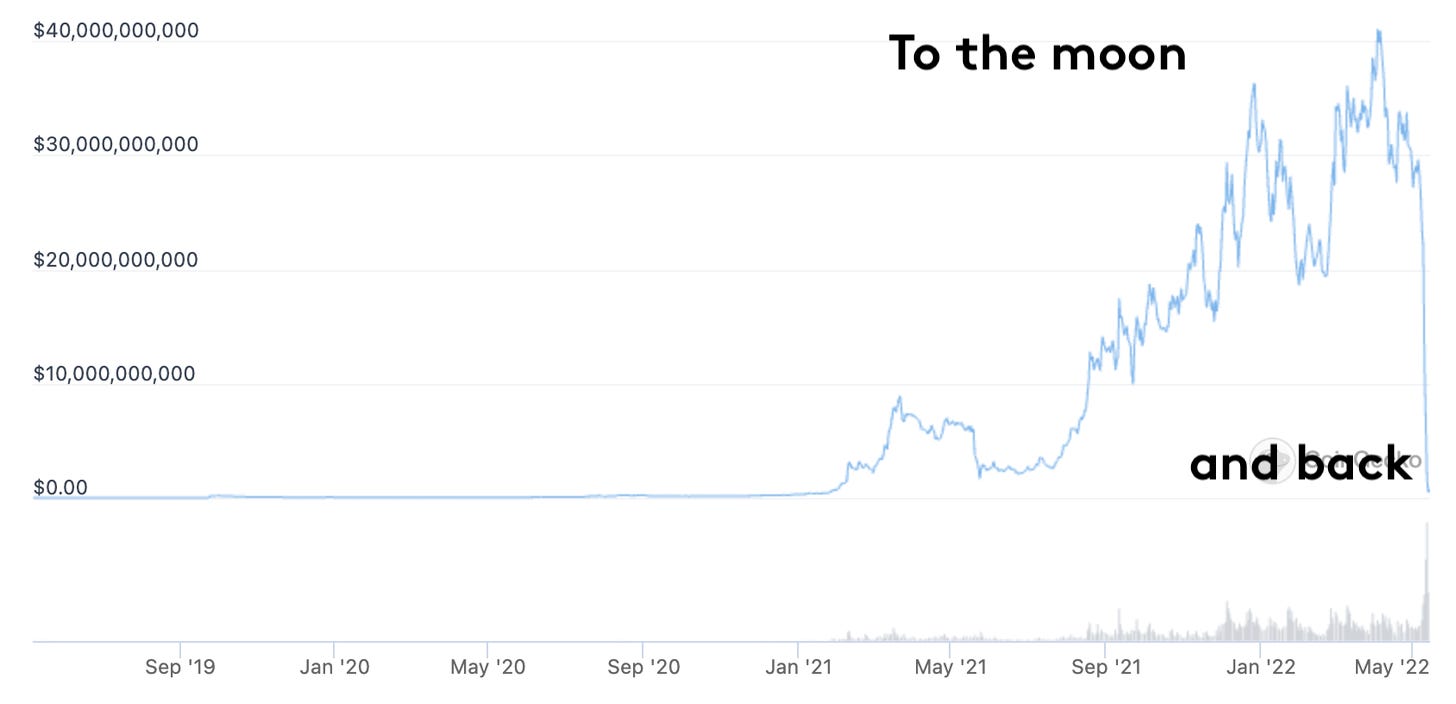

To the moon and back

A quick recap of the story:

There are three key elements:

UST (stable coin)

Terra (blockchain) and its Luna token

Anchor lending and borrowing platform on Terra

Terra is a range of stable coins pegged to various currencies, but the main one was UST (USDTerra) pegged to the USD. It reached a market capitalisation of $40bn, then collapsed. Instead of relying on collateral, the peg was maintained by an algorithmic process.

(NB: I say Terra IS not WAS because the protocol is still alive, although worthless.)

Alongside Terra, there’s Luna.

To maintain the price of Terra, the Luna supply pool adds to or subtracts from Terra’s supply. Users burn Luna to mint Terra and burn Terra to mint Luna, all incentivized by the protocol’s algorithmic market module.

There was a whole Luna ecosystem of apps, but here we only need to know about the Anchor Protocol, where you can lend and borrow. Lending was incentivised, and you could earn a yield of 20% on your UST pegged to the USD.

(NB: I use the present, not the past, because the protocol is still alive, although worthless.)

Why was the total supply of UST worth $40bn? Because people decided to exchange $40bn worth of their assets in exchange for UST.

Why did it go to 0? Because it was backed by Luna, which was not backed by anything (I’m skipping the late attempt to add Bitcoin as collateral).

At its peak, the market capitalisation of Luna was $18 billion. It became the 7th largest crypto project for a brief moment

Were the investors Lunatics?

Yes, because that’s what they were called. Some even got a tattoo.

But no, they were not insane. We can all potentially be Lunatics.

It was not just '“dumb” money. VCs, successful investors like Novogratz (above), or the Head of Research for the popular Real Vision platform, Remi Tetot (below), all backed the projects.

The above tweet deserves a pause. It’s from the “Head of Research” of a platform where you can gain an understanding of the complex world of finance, business and the global economy. Yet, he had 100% of his crypto assets in one token, without any risk management.

The journey to the Moon

The rise of Terra is a case study in cognitive bias.

For Sam Bankman-Fried, the CEO of FTX, it’s a case of probably “bad marketing”.

It’s an interesting choice of words. Maybe it’s an attempt to criticise the project without alienating the community.

It’s the marketing that was bad. And by bad, we mean excessively efficient and impactful.

But that can’t be the whole picture. Marketing can help more users find a good product. It can slow the decline of an average product. But it can’t transform an idea into magic internet money. Only our brains can make it happen.

The most valuable lessons from Terra point to our cognitive bias. Although the overall crypto enthusiasm made it a fertile ground, these are not crypto-specific.

in “Thinking Fast and Slow”, Nobel Prize Winner Daniel Kahneman highlights cognitive biases that can be applied to the success of Terra:

What You See Is All There Is

Herding

WYSIATI

Kahneman introduces the concept he terms What You See Is All There Is (WYSIATI).

This is often an optimistic bias, which makes us believe that what we have observed in the past will also work in the future without correctly assessing the risks or considering chance.

The user experience of UST from most of its history until May 2022 is a positive one. That includes mine (here are my transactions for transparency):

I exchanged GBP for UST via Transak, a fiat to crypto ramp embedded into the Anchor Protocol: lower fees and smoother experiences than any other on-ramp (the fees were subsidised)

I deposited UST in Anchor at around 20% APR

Then withdrew and convert back to fiat at par (until 9 May 2022)

It worked really well until it didn’t. I’m sharing my personal experience to emphasise the power of WYSIATI. I was fully aware of the nature of the protocol, and I placed a small sum which I withdrew safely at the first signs of nervousness. I did it partly as an experiment. But looking back, this was not a risk worth taking. I knew it was not worth it, but watching this very stable UST/USD chart and the 20% APR was irresistible.

For many people, “all there is” was a straight line for the price of UST vs USD and 20% APR.

But for others, it was much more than that:

Herding

We rely on size (or market cap), community, and endorsements to guide our choice. This is a rational and efficient approach, at least in the first steps, but:

Size is not a security guarantee: If you look for stablecoins, the starting point is to rank them by capitalisation. UST was on investors’ radar because it was the second-largest stable coin.

Some Defi experts warned of the dangers of UST, but overall the call from crypto influencers (there’s a long list to add to Novogratz and Tetot) was very bullish.

Cult-like leaders represent an additional risk: here’s an example of Do Kwon’s style. (The tweet was posted as the collapse of UST had begun, but the price was still close to par).

The terra community is (still) large and active. On Reddit, heartbreaking stories have replaced the memes.

There were thousands of people building promising protocols on Terra. There was a leading ecosystem of crypto applications that could have flourished - if Terra was sustainable. In a sense, Terra was a modern-day utopian community.

What does it mean for Defi?

It’s still early, but let’s compare it with famous bankruptcies and crises.

Terra is not the Enron of Crypto

Enron also reached the #7 spot before collapsing ($70 billion market cap at its peak). But this is very different.

Terra was built transparently and openly, unlike Enron or Theranos, which misled investors by hiding or falsifying information.

It’s often compared to a Ponzi scheme because of its self-sustaining mechanism, but there is no sign that Do Kwon and the Terra team set out to defraud investors. (Although a story of missing Bitcoins is emerging).

The design was inherently bad. There were Blockchain-specific risk management failures (collateral, liquidation, governance) in the Terra project. Yet it was not a blockchain failure, hack, or lousy code that crashed the protocol.

The fact that it was built on the blockchain made it easier for investors to understand the project's true nature. Many choose to ignore it.

Enron had fake holdings and off-the-books accounting practices. It used special purpose vehicles (SPVs) to hide its mountains of debt and toxic assets. Its collapse showed the hazards of creative accounting and financial engineering.

I don’t think Terra showed the hazards of Defi.

It doesn’t look like a Lehman

In his newsletter, Henri Arslanian, a leading crypto commentator and previous guest on the podcast wrote:

In the same way that we saw the effects of the Lehman Brothers crash for over a decade in traditional finance, the same will be true in crypto markets.

The correction in the crypto markets has been sharp, and we can expect some more casualties to emerge. But it doesn’t look like there is any systemic risk. The regulators do not look like they are hurrying to step in.

There have been outflows from USDT, but they have mainly benefited USDC. There is no contagion to other stablecoins backed by collateral. (Although I must add that I am very cautious about USDT - but more on that another time).

There were some outages on other chains, but overall the Terra collapse seems isolated. I would even be cautiously optimistic and say that the Terra collapse has demonstrated the resiliency of Defi. If a major chain can collapse without affecting the whole crypto universe, then it’s a good sign?

More surprisingly, other projects with a similar mechanism as Terra look still alive and well. I’m thinking for example of the coin called “Magic Internet Money” by “abracadabra.money”.

I don’t make this stuff up. There could be a lot more of those, they may survive, reform or disappear but either way, Defi will be fine.

Nobody’s going to the moon anymore

Terra’s collapse is not about crypto. It’s about the cognitive bias that governs investors. Herding and WYSIATI are nothing new. Combined with excessive liquidity and crypto optimism, they brought Terra to the moon, and market reality brought it back.

I still think there’s an alternative universe where Terra succeeds. In that universe, instead of using their Luna coins to buy Bitcoins as a reserve, as they did a few months ago, they buy US Treasuries. And they keep buying until gradually UST transforms itself from “magic internet money” into “fiat-backed sustainable stable coin”. The fiction sounds a lot more boring than the reality. But that’s where Defi is heading.

For investors, that means no more going “to the moon”, but we need to learn to appreciate earthly returns.

Some other stuff that may interest you:

On the podcast, we discuss inclusive design in fintech and asset management in web3.0

On YouTube, we talk about the Private Equity hype and paying in crypto