Ramify & the new digital ways of milking investors

It looks like Wealthtech won't save us after all

Hi! It’s George from Investorama - Separating investment facts from financial fiction. The Ramify news (French Wealth startup raises €11M) sent me here.

I started my career in finance, selling structured products, derivatives and alternative funds to institutional clients across Europe. While I was enjoying the job, travel, and sophistication of the products, I would tell family and friends not to buy them.

I only realized the moral implications years later. When you’re in a commercial job, you see things differently, but I was happy to turn that page when I launched a media business. I remained interested in financial markets, for myself and from a distance, until Fintech sparked my interest again 5 or 6 years ago.

I’m attentive when I hear of a new fintech launch or raise in the wealth or investing space because I’m hopeful that someone will come up with a better solution for investors. I hadn’t heard of Ramify before so I was eager to check them out.

What I didn’t expect to see there was the most old-school marketing tricks to push high-margin products to unsuspecting investors.

Below are three textbook examples taken from the Ramify website (in French):

Remember I’m not judging the products but the way they are marketed.

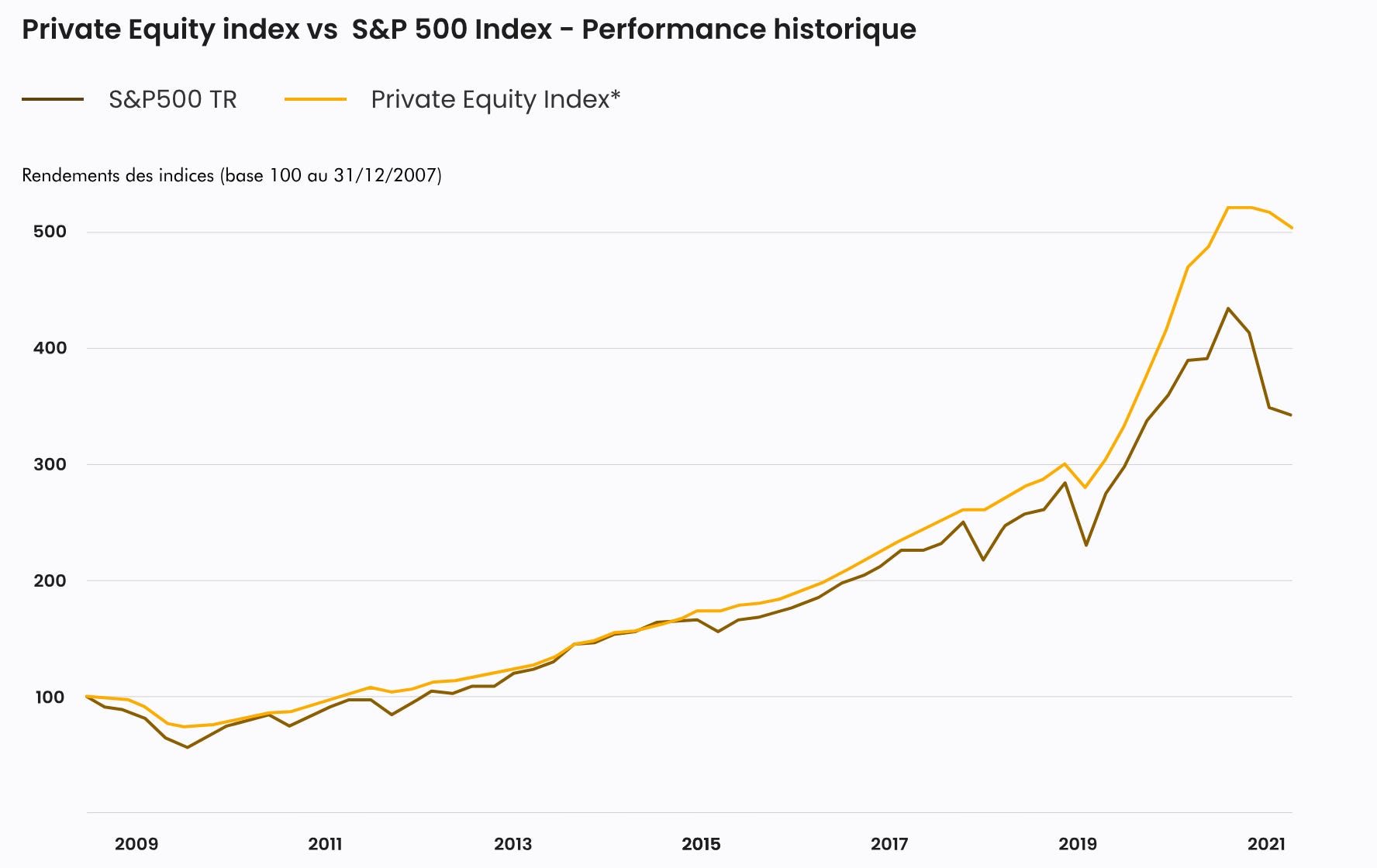

Optimal date selection

Here’s the chart for their Private Equity (PE) offering page.

I won’t argue here over PE’s historical ‘outperformance’ (I’ve done it before), or the choice of PE Index (Preqin’s PE Index). No, what’s striking here is the start dates on the charts: December 2007 to something that looks like mid-2022.

In other words, the previous top and the most recent bottom, presenting the worst possible outcome for the public equity index. The website team will not rush to update this 2-year-old chart.

Fantasy IRR numbers

Here’s a screenshot from their Art offering. TRI in French means IRR, or Internal Rate of Return (also an Inappropriate Return Ratio).

Again, this is not about judging whether investing in Art is a good idea (I’ve covered Masterworks before), but its marketing. Specifically, the fact there are three scenarios:

‘Contexte favorable’ = favourable (or optimistic) case

‘Contexte moyen’ = average (or base) case

‘Défavorable’ = unfavourable

They form a range from 34.25% to 11.85%. Based on what? We don’t know. But expressed in words not numbers, I’d say the range goes from fantastic to great. No room for negative thoughts or negative returns here.

High fees, but with climate in the title

Here’s their structured products offer:

It’s a 10-year(!) product that will redeem after a year and quarterly if the underlying closes above its initial level on observation dates. That’s the positive scenario where investors will get a coupon equivalent to 9% p.a. The downside is not fully protected, the capital is at risk if the underlying drops by 50%.

There are more interesting details here, I only wanted to give you an overview in English. For now, you will have to trust my structured product experience when I say THIS PRODUCT IS FULL OF FEES!

Ramify also offers more traditional products, but I feel I’ve seen enough to understand the core of their business model: to sell very high-margin products to more digital audiences.

And that worries me about the Fintech/Wealthtech sector. There’s a lot to improve on what legacy brokers and wealth managers offer. But it’s hard and expensive. Is there a way to do it without pushing high-fee products?

End of rant (for now).

great coverage as always, glad to see also coverage separating investment facts from financial fiction ... kudos to your mission! Cheers!