Who needs correct valuations when you've got love?

Part 2 of a mini-series on BREIT and the marketing genius of Blackstone.

Hi! It’s George from Investorama - Separating investment facts from financial fiction. Storytelling is great for marketing, but there’s a fine line between storytelling and fiction. Blackstone is crossing it with BREIT - but they do it in style.

BREIT doesn’t make financial sense

In Part 1, I wrote about BREIT, being one of the most successful funds in history, despite raising huge concerns. The Blackstone Real Estate Income Trust Fund a unique fund marketing success story that transformed a foray into a new market, individual investors, into Blackstone’s greatest revenue generator.

Since then Phil Bak (who I interviewed initially about BREIT) published the Big Bad BREIT post, is a very comprehensive analysis that I highly recommend. I’ve also referred to another guest on my podcast Nicolas Rabener who had used BREIT to build a case against private markets. And he followed up with a post that brings to life what may eventually happen to BREIT.

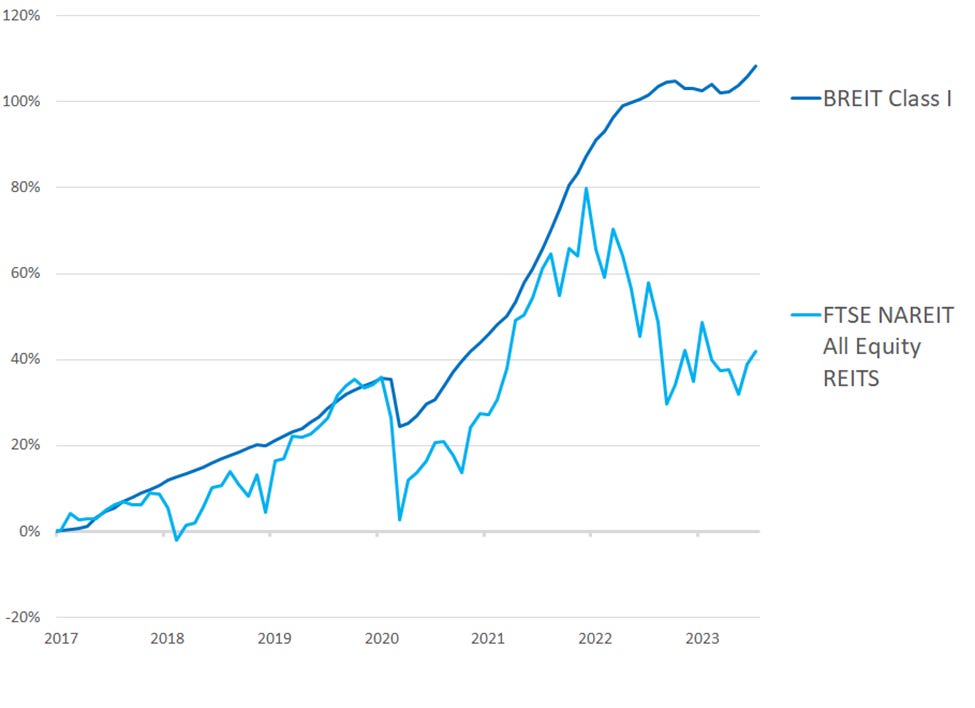

Gradually…. the fund’s NAV rose until it peaked in 2023, then declined slowly.

Then suddenly… in June 2024 it was reset to a 21% yearly drop.

If you look at BREIT’s chart, this is not a crazy scenario.

There are objections to this comparison and answers to these objections in Phil’s post. The conclusions are the same as articles from Business Insider, the FT or the NYT, and countless independent publications: the fund appears grossly overvalued.

The natural next move for investors in the fund who read those papers would be to redeem their shares as quickly as possible.

But that’s not what’s happening. BREIT’s inflows had a record quarter and they exceeded redemption requests, allowing to meet all withdrawal requests.

So what’s happening here?

BREIT makes marketing sense

Let’s assume you’re a BREIT investor, this fund is targeted at wealthy individuals and distributed via advisors who take a commission upfront. You’re not taking an active approach to investing. The main draw of the product is its regular income, and the whole idea is to relax about it.

You don’t read the articles above, I think that’s an important assumption, otherwise that doesn’t make sense.

But you still get regular updates via Blackstone directly or indirectly, via an advisor.

And what you see month after month is:

Steady income

Stable or gently rising valuations

It’s a great customer experience!

It doesn’t matter if:

The fund is paying more dividends than the income from properties

The fund has entered a costly deal with the University of California, which injected $4 Billion as an emergency cash injections

It’s impossible to sell those properties at the NAV price

It’s the number one lesson for startups: design a product that people love. In fund management customers (investors in this case) love: high income and/or returns.

The problem in finance is that you can’t manufacture that with investing products, but can you still manufacture love?

Remember it’s not about the characteristics of the product, but about the experience it delivers. What if we could create a fund that makes people feel richer, happier, etc?

Manufacturing product love (“fundzi”)

I see 2 options:

Technically, you can deliver perfectly smoothed returns as long as you keep getting new money. That’s what Madoff did. It is called a Ponzi scheme and it is illegal, that’s a problem.

(There are also a few practical problems even if you don’t get caught).

A more normal choice is to invest in assets that MAY deliver great returns but come with risks.

If the assets go down, like real estate did, you can say to investors:

You've invested in a real estate fund. The overall market is down. We've done well/outperformed/ tried hard (pick one or more), so you should be quite happy.

Maybe “Unilmmo: Wohnen ZBI” said something similar to their investors as they marked the fund down.

Some investors may be upset about that. Some others may have understood. Those that saw it coming would have tried to exit early and maybe that’s what triggered the downgrade. I don’t know any details, but I ‘m sure it didn’t bring them… love.

The ongoing love for BREIT can only be explained via a hybrid model.

Of course, it’s not a Ponzi scheme.

BREIT really invests! The properties are real, and we discussed some of them in detail with Phil Bak, these are good properties! Their value has dropped, but it should not ruin the customer experience.

But we also know that investors can redeem their shares and crystallize their gains only because of the cash injection from the university and the new inflows. That sounds a lot like a Ponzi scheme.

A Ponzi scheme is an investment scam that pays early investors with money taken from later investors to create an illusion of big profits.

What do you get when you mix the smoothing characteristics of an investment where outflows can be matched by inflows and the potential upside potential of risky assets?

A product that delivers a wonderful customer experience to income-seekers! You’ve designed for love!

To design such a product you need:

private assets

packaged in a perpetual structure

semi-liquidity (gated liquidity)

a great marketing engine for net inflows

Blackstone has all of that and more

We need a name for this type of hybrid product, for now, let’s call it a “fundzi”. (I’m sure we can find a better one).

The end game

For the avoidance of any doubt, dear reader, I DO NOT RECOMMEND CREATING OR INVESTING IN A FUNDZI.

The outlook for BREIT can be very dark. Here’s the conclusion from one of the Business Insider contributors:

In the absence of a market price, independent accounting and tighter government regulation are needed to ensure that investors have the accurate, verifiable numbers they need to make informed decisions. With private funds like BREIT, too much maneuvering takes place in the dark. And if history is any lesson, the dark is a very bad place to be doing business.

Finominal outlines 2 possible outcomes:

Perhaps real estate valuations will increase and Blackstone will get lucky by being able to avoid a drawdown in BREIT.

However, more likely is that BREIT’s external appraisers, which theoretically are independent but practically are conflicted as they get paid by Blackstone, will slowly decrease valuations to get these closer to the market. If that leads to an increase in redemptions, then this will likely result in steady losses in BREIT as Blackstone is forced to sell and write down the portfolio asset by asset.

I think most commentators point at option 2: BREIT may eventually end up like “Unilmmo: Wohnen ZBI”: forced to revalue sharply.

But I don’t believe in a scenario of gradually decreasing valuations leading to redemptions - not for a long time.

The time factor is critical here. We’ve been focused on BREIT so far, but let’s zoom out. What is at play is much bigger than the $120bn BREIT fund. Blackstone sees an $80T private wealth opportunity.

Next to BREIT (real estate), there’s already BXPE (private equity) and BCRED (private credit).

BREIT is the oldest, largest, most profitable of a series that will expand. It’s the poster child for the “democratization of alternatives”.

A “Unilmo” scenario for BREIT: gradual depreciation of assets - followed by redemptions - then sharp devaluation - would kill the customer experience, but more importantly it could stop the whole movement.

They need more time to consolidate the channels and expand products, structures and distribution channels.

That’s why I think it’s unlikely to see a depreciation and even less likely to see dividends reduced. I don’t know how it’s going to work, but expect Blackstone will put up an enormous fight and use all the possibilities of the “Fundzi” structure to keep that opportunity opened… until a $100 billion fund that brings in nearly $1 billion in fees doesn’t seem that important any more.

PS: after hitting publish the name “Fundzi”, reminded me of something or someone. Of course, the “coolest” fund needs to be named after the coolest guy!

If you don’t know what I’m talking about, check this out.

quite a case ... thank you sir!